Macro Monday: Survive 2022 and everything will be alright.

The consensus on the economy looks negative, it shouldn't be.

Nugget: The top quintile, by household income, account for 34% of spending in Australia.

The view that the global economy is hurtling towards a hard landing in the midst of rising inflation and interest rates is now consensus. Lessep’s view is different. If the global economy can weather 2022 (it will), 2023 and beyond shape as years of solid expansion driven by an easing of inflationary pressures and increased investment in supply chains and the post-pandemic world.

This view is outlined below, both conceptually, and using Australia as an example. Unlike other major developed economies, Australia experienced the steepest rate cycle in the wake of the Global Financial Crisis. This period offers important lessons for investors today.

Conceptually

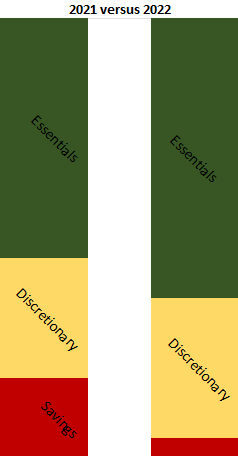

What were households doing in 2021, and what can be expected in 2022?

The diagram below, vaguely based on RBA data from 2009, lays this out. Household spending on essentials will increase in 2022 (inclusive of inflation and interest rates), in this example by 20%. Savings will fall from 20% to 5%, allowing discretionary spending to increase by 17%; a solid boost for GDP growth and employment. Given last year’s restrictions, and accumulated savings of $436bn (20% of the economy), Australian households should be able to cope with price increases and raise spending, at the same time.

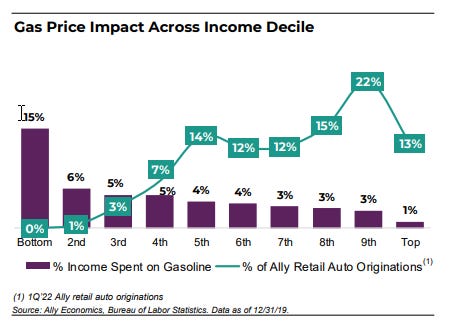

Arguably, the situation is even better than this, with affluent households remaining largely unaffected by goods inflation, as evidenced by Ally Financial’s chart below. According to the ABS in Australia, the top quintile of households by income account for 34% of all consumption spending.

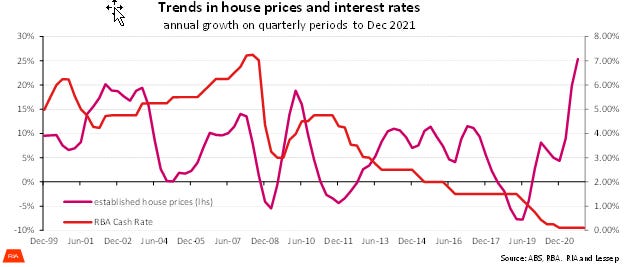

Australia in the Wake of the GFC

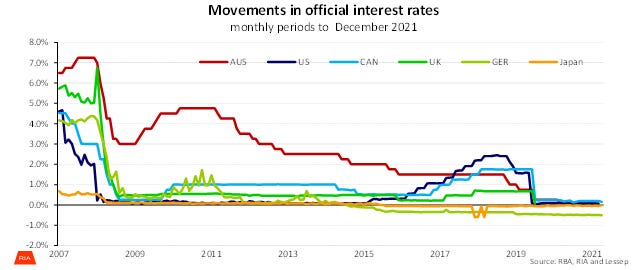

It is true that Australia’s financial crisis in 2008/09 was limited. Employment remained strong at the height of the crisis, and the economy was able to expand as financial markets and China’s growth improved. The RBA raised its cash rate by 175bps from September 2009 to November 2010 as it withdrew emergency policy support. The withdrawal of emergency policy support is analogous to global monetary policy settings today.

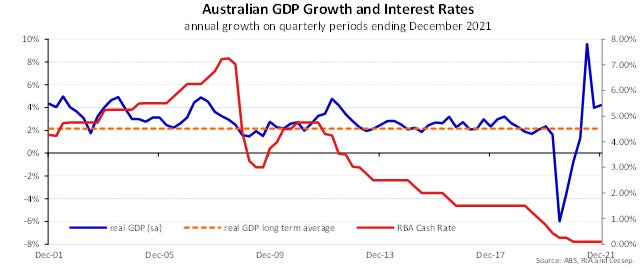

From a growth perspective, it’s likely that raising rates did slow the post-GFC recovery, but as the chart below shows, growth remained at or above average during the tightening phase. The global economy and markets would be happy with average growth in 2022.

The biggest impact on the economy came in a sharp decline in house price growth. House prices peaked six months after the beginning of the rate hiking cycle and fell 5% over a period of 21 months. Importantly, as rates peaked, house prices began to accelerate again. This suggests 2023 will be a strong period of growth for US homebuilders.

After a 35% increase in house prices in Australia from June 2019, it’s likely that this tightening phase by the RBA will have a more substantial, but manageable, impact on house prices.

Broadly, Australia weathered the removal of emergency monetary policy well. Households expected the changes and had a stock of savings to get them through. (The decline in interest rates from 2011 reflected a policy shift by the RBA that focused on currency depreciation, rather than a weak economy). The evidence suggests a return to higher interest rates is manageable for the global economy coming out of the pandemic as well.

The Outlook

2022 is a tough year for the economy as prices rise, policy changes, and uncertainty make decision making difficult. But if the combination of high savings, and the desire to return to normal, support consumer spending in 2022, the global economy can expand more sustainably in 2023. Businesses in 2023 will benefit from clarity as regards the extent of the interest rate cycle and the opportunity to invest in supply chains and the post-pandemic economy. Households will see cost of living pressures stabilise and consumer confidence can improve. Again, current market prices are an opportunity.