Snakes and Ladders, Pipelines and Tankers

Snakes and Ladders, Pipelines and Tankers

Buying Teekay, TORM, International Seaways and DHT Holdings

The disruption to global trade as a consequence of Russia’s invasion of Ukraine poses a challenge to the global economic order. The likely outcome is for a re-stacking of global trade supply lines that favours mobility over fixed infrastructure. The permanence of these changes will be dependent upon the rate at which Russian resources are plugged back into the system.

Global trade is in many ways analogous to a jigsaw puzzle. The puzzle pre-January 2020 reflected a highly refined, interconnected system that met the world’s demands for resources. Covid led to the jigsaw’s pieces being spread to the wind and as they were re-assembling, Russia invaded Ukraine. This is the greatest challenge to the system in three decades.

Over the course of 2022, the scattered pieces will return to places vaguely resembling the pre-March 2022 puzzle in terms of outcome rather than efficiency. We will be fed and provided with energy but at a much higher cost. Current assets like pipelines will stand empty and tankers will shift into over-drive. To mix metaphors, the new puzzle will feature snakes (pipelines) and ladders (tankers). Consequently, tankers represent an important short-term opportunity.

Typically, the tanker industry is uninvestable. The volatility in day rates makes the equity of companies in the sector unattractive. Unattractive equity means debt-funding and perennial balance sheet issues. But the current market conditions, which seem to indicate a sustained rise in prices, offer investors an opportunity to capture short-term gain to offset rising price pressures in other sectors.

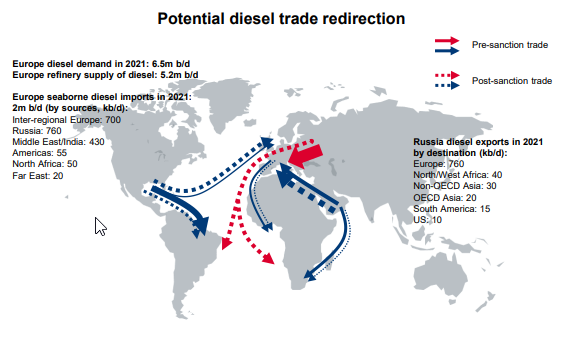

Recent presentations by tanker companies highlight the challenges for global trade and the opportunities for tanker companies. The Danish company TORM $TRMD outlines the re-allocation problem. Europe consumes 17mn barrels of oil p/d. 3 million comes from Russia, largely via pipelines. This will be replaced by other producers via tankers. TORM also suggests Iran’s re-entry would require further tanker capacity.

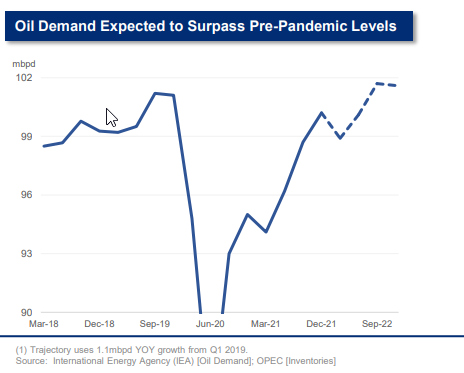

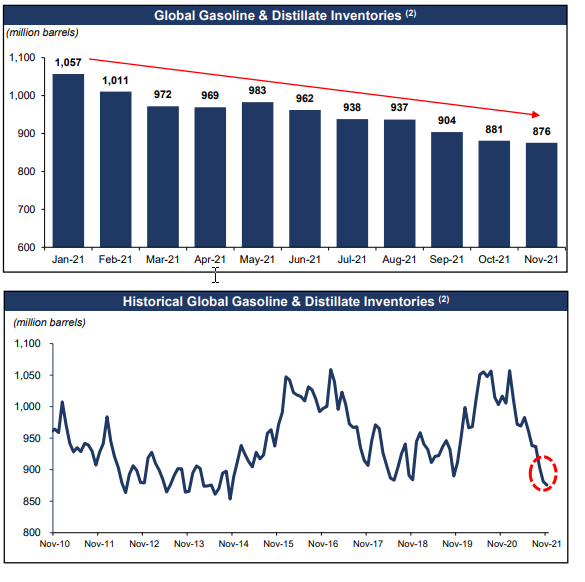

This increased demand for tankers comes at an opportune time for the industry. Across the board, investor presentations prior to the invasion reflected an industry with a hopeful (read desperate) outlook focused on a return to pre-pandemic activity levels and low inventories.

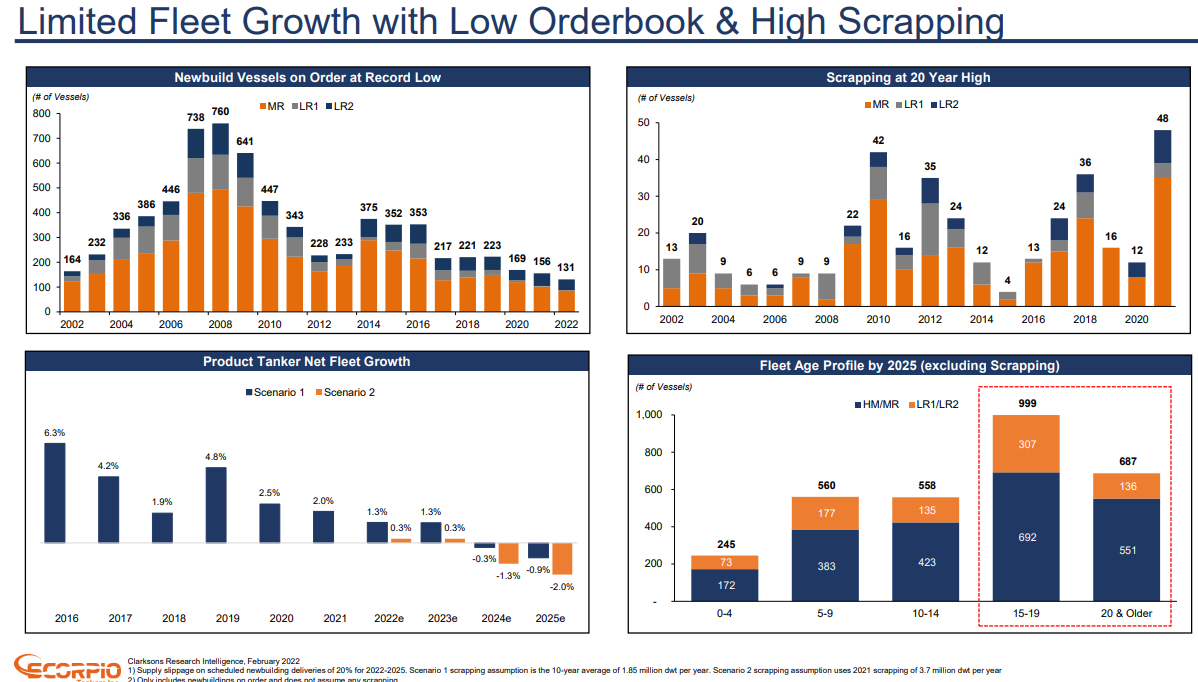

Companies highlighted a weak competitive environment with low new ship orders, high scrapping rates, and an increasingly elderly fleet.

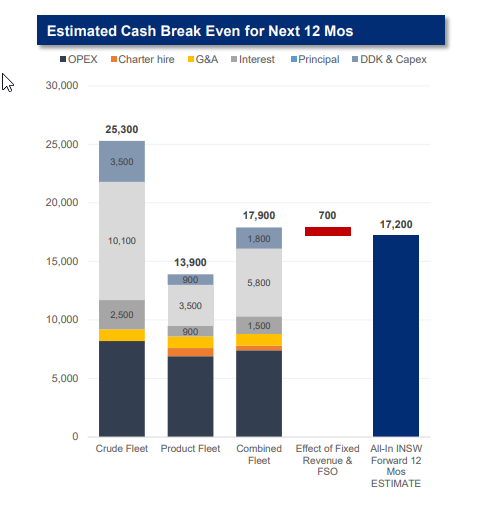

Against this hopeful backdrop, companies are keen to share cash break-evens ranging from $8,500 at TORM to $17,200 at International Seaways. With current day-rates above these levels and likely to improve further, tanker companies will be in a position to make super-profits and return funds to shareholders.

In this environment, I am happy owning a basket of tanker operating companies. My current basket includes Teekay, International Seaways, DHT Holdings and TORM.

The length of the trade will be dependent upon the path by which Russia is re-integrated back into the global economy, particularly the European Union. This may not occur. But the costs to be inflicted on European households are such that some sort of resolution is likely to be required, particularly before the winter of 2022/2023. Already, Hungary, and now Austria, have shown willingness to entertain the possibility. Austria’s Chancellor is currently (11th April) in Russia. But even a short period of high prices would support improved prices for the sector.