Software: Chiaroscuro

Software 101: Episode 3

The concept of chiaroscuro uses light and shadow as contrasts to create clearer visual imagery. As the software series resumes, this concept makes clear what is a software company and what is not.

Three aspects of the software or SaaS business model were introduced in Episode 2:

ARPU (Average Revenue Per User) that grows as the network grows

Gross Margin that grows as the network grows

Churn that falls as the network grows

The consequence is the most profitable business model in history.

The current market for technology stocks is bringing this contrast between a SaaS and non-SaaS business into stark relief. True SaaS businesses are down 35-50% from all time highs. Non-SaaS businesses are down 80-90%.

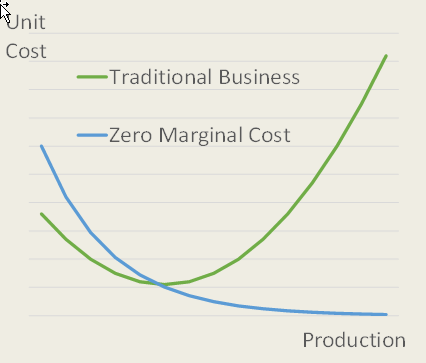

The most important theme in this critique of non-SaaS businesses is the physics of a byte economy and an atom economy. A byte economy has no constraints on growth while an atom economy has clear constraints. These constraints limit growth and profitability.

In the spirit of chiaroscuro, the contrasting, non-SaaS businesses, will be some of the darkest and most egregious examples: Peloton (90%), Zillow (-71%) and Shopify (-81%).

ARPU

The ARPU cycle for a SaaS business is virtuous; more clients, create more data, a better product, driving more clients. SaaS businesses are zero marginal cost. For atom constrained businesses there are limits on how far a business can grow before new clients become marginal. Zillow’s Zillow Offers scheme was designed to buy, for cash, homes listed on its website. This saves the client selling and repair costs. But as Zillow gets closer to the median priced home, it’s revenue per user falls because the opportunity for profit declines. It’s the market for lemons.

Gross Margin

Gross margin for software firms is the key performance indicator. In the fullness of time, the true SaaS firm will approach a gross margin of 99%. The combination of pricing power and scale benefits, creates constant gross margin expansion. ServiceNow has expanded 14ppts in seven years, Xero 12ppts in the same period, and Salesforce.com 6ppts, despite pursuing expensive acquisitions.

Shopify, in contrast, has pursued a fulfilment strategy that has seen its gross margin fall from 59% in 2014 to 52% today (despite the tailwind of pandemic e-commerce growth). It’s likely that as it extends its fulfilment strategy, Shopify’s gross margin approaches Amazon’s gross margin of ~40%, a further 12ppt fall.

A key risk for Shopify will be the increased competition for resources that characterises the atom economy. In the atom economy, no matter how great a business is, it becomes constrained by the activity of its competition. The greatest homebuilder, consistently delivering superior product to clients, faces approximately the same resource constraints for land, lumber and labour as the worst. For Shopify, it will begin to compete for land, labour, vehicles, and, over time, the infrastructure it uses to ship goods to customers.

Not only will this lead to a lower gross margin but it will contribute to a bigger balance sheet. Total debt at Shopify has risen eight-fold since 2019. SaaS companies, by contrast, are all negative net debt.

Churn

SaaS customers don’t leave. As Xero shows, its churn has been ~1.1% per month and fell to 0.88% in the first half of 2022. Customers don’t leave for a number of reasons: low cost of SaaS solutions and the storage of data in the cloud are important. The key reason, however, is productivity. In SaaS businesses, there is no longer an alternative or better solution to the process problem than the SaaS solution.

The non-SaaS technology darlings never offered this productivity solution. They were good ideas, relatively well executed, and capable of taking market share. But they were never capable of becoming the universal solution. Peloton with gyms, WeWork with offices, Airbnb with hotels, and Uber with taxis, are all examples of a good solution but not a universal solution. As a consequence, they fight for resources and they fight for customers.

For Peloton, there will always be alternatives; the gym, the park, or the hockey field. As such, its churn will be higher on an annual basis as clients shift between the various alternatives.

Conclusion

One day this market for technology stocks will turn; likely sooner rather than later. As the market turns, the true SaaS businesses will shine and the non-SaaS businesses with falling profitability and weakening balance sheets will struggle. For the Lessep IM Global Equity Portfolio these true SaaS businesses are (ordered by the biggest to smallest daily portfolio loss on 12th May 2022):

Xero

Atlassian

Adobe

ServiceNow

Intuit

Microsoft

The Trade Desk

Autodesk

Dubber