Software: Outlining Valuation

Software 101: Episode 4. Why paying 14x Sales for SaaS is reasonable.

The previous episodes of Software 101 outlined the unique profitability of the software or SaaS model. The next few episodes will look at valuations of these companies.

Eye-watering Valuations

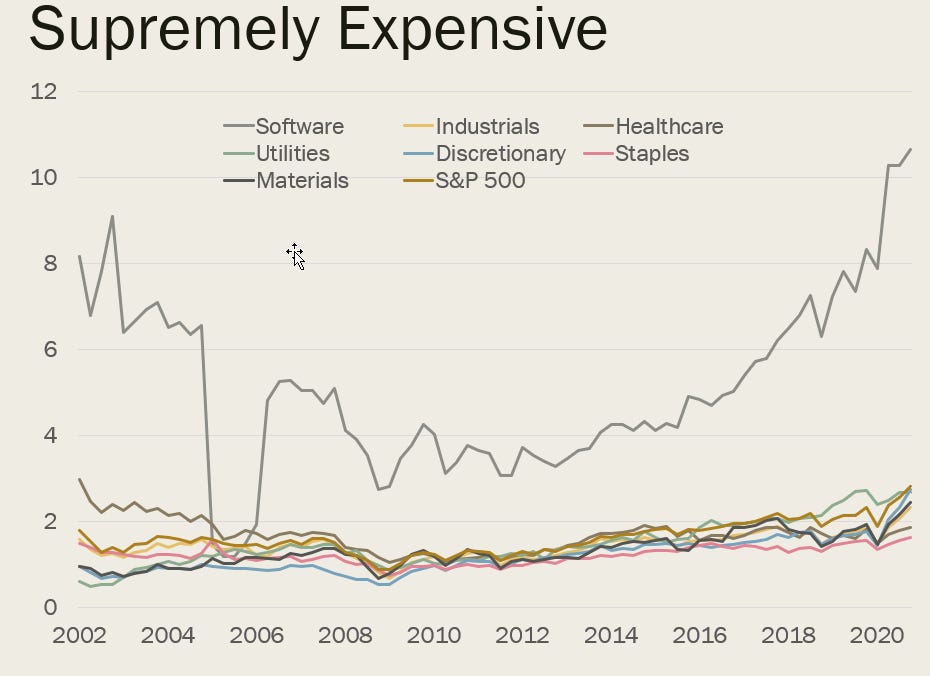

Below is 20 years of price to sales data for companies across the S&P 500 by sector. Software is 5-6x more expensive than every other sector. Are software investors dumb, or has the market found something it truly likes?

Investors will look at software valuations and baulk. The extreme nature of their valuations, relative to history, will make the average dialectical gaussian shrug shoulders and move on to the next opportunity. In reality, however, the market is looking ahead to what a mature SaaS business will look like.

Paying 14x Sales for a Company

Through the lens of ServiceNow, it is useful to dissect what an investor is receiving, in the long-term, when paying 14x current year sales for a share in the company. From a financial perspective, what does a mature SaaS company look like?

Currently, ServiceNow makes a meagre 37 cents a quarter on a share price of $432. But long-term, its possible to assume, ServiceNow will earn more than 80c on every dollar of sales in gross margin, and half that, 40c, in Net Income. If ServiceNow wanted to stop growing, they could do that now, and earn ~$12.34 per share and trade on 35x current earnings. This is not an unreasonable valuation.

If these assumptions of profitability are projected forward with different revenue growth rates, it’s possible to make some simple, back of the envelope calculations, about current opportunities in the software space, as represented by ServiceNow.

Only if revenue growth were to average 10% for the next three or five years, would an investment in ServiceNow represent a negative NPV on today’s price. On most outcomes, ServiceNow represents a positive NPV over the next three to five years.

This model rests on relatively unaggressive assumptions; a discount rate of 10% (ServiceNow’s historic cost of equity is 8.6%) and a target PE Ratio of 28.6x current earnings, the long-term average of Microsoft (from 2016 it’s averaged above 30x). Further, as a simple model, it takes no account of share buybacks. Currently, ServiceNow generates $1.8bn in Free Cash Flow (or 51x FCF); most of which can be allocated to buybacks.

But it highlights why investors, looking out over the long-term, can see value in software stocks. Particularly, if investors believe SaaS companies are the most uniquely profitable in financial history and the path to maturity is stable.

The Big Assumptions When Valuing Software

At the core of this methodology are a couple of important assumptions that need more explanation. First, revenue growth is stable. Second, SaaS companies don’t require new capital.

The next episodes in Software 101 will explore these assumptions in more detail.