Software: The Business Model

Software 101: Episode 2

Episode One of this series, argued that software is economic infrastructure. It facilitates more efficient economic activity at a fraction of the price. Similarly, it requires large upfront costs but is extremely profitable at maturity. But in contrast, there are no capacity constraints, limited regulatory oversight and no financing risks.

The pay-off from being the economic infrastructure of the 21st century is enormous. But as Bill McDermott said in 2018:

“Since 2000, there were 4,500 companies in the IT industry that took a Series A investment, only 75 made it to an IPO, only 36 became dominant category winners. Those winners now own 76% of their entire addressable market…”

There are only a few winners. Here in Australia Xero, alone, meets the business model requirements to be considered economic infrastructure.

Software or SaaS business models that meet the definition of economic infrastructure are complicated, highly engineered businesses that offer their customers a unique and simple solution to a process problem. For users, it’s cheaper to pay for SaaS solutions than to not pay. For the SaaS business, the end goal is a zero marginal cost for both production and sales. This results in fast, consistent revenue growth and the highest profit margins in history.

The SaaS Economics Equation

The effectiveness of a SaaS business model can be measured and assessed through the following equation:

Life-Time Customer Value (LTV) / Customer Acquisition Cost (CAC)

LTV = ARPU x Gross Margin x Churn

CAC = (Total Marketing Costs/Gross Additions)

The higher the ratio, the better the company. Xero produce this data on an annual basis. In its ANZ business, the ratio is 13.2, where long-term customer value is $3,682 and the cost of acquiring the client is $279 (expanding marginal returns). By contrast, its international business has a ratio of 2.7 where long-term customer value is $1,608 and customer acquisition costs are $596. A lack of offshore scale drives lower customer value and higher acquisition costs.

Average Revenue Per User

ARPU within SaaS businesses is driven by the three-way fly-wheel of solution, users and data. As a company creates a software solution that attracts users, users create data that improves the solution, and attracts more users. The data acts as a competitive advantage in solution development and forms a barrier to entry. Further, process mining, using the data to identify new uses for the software, can become a two-way street, with users creating new use cases for the software.

For Xero, ARPU in ANZ is $31.23 and has risen 5% per annum since 2019.

Gross Margin

Unlike traditional businesses, including economic infrastructure (i.e. the cost of increasing the capacity of a fully utilised road), SaaS businesses trend towards zero marginal cost of production. As businesses mature, gross margins can approach 90% or higher. Xero’s gross margin has increased from 65% in 2013 to 87% in 2021.

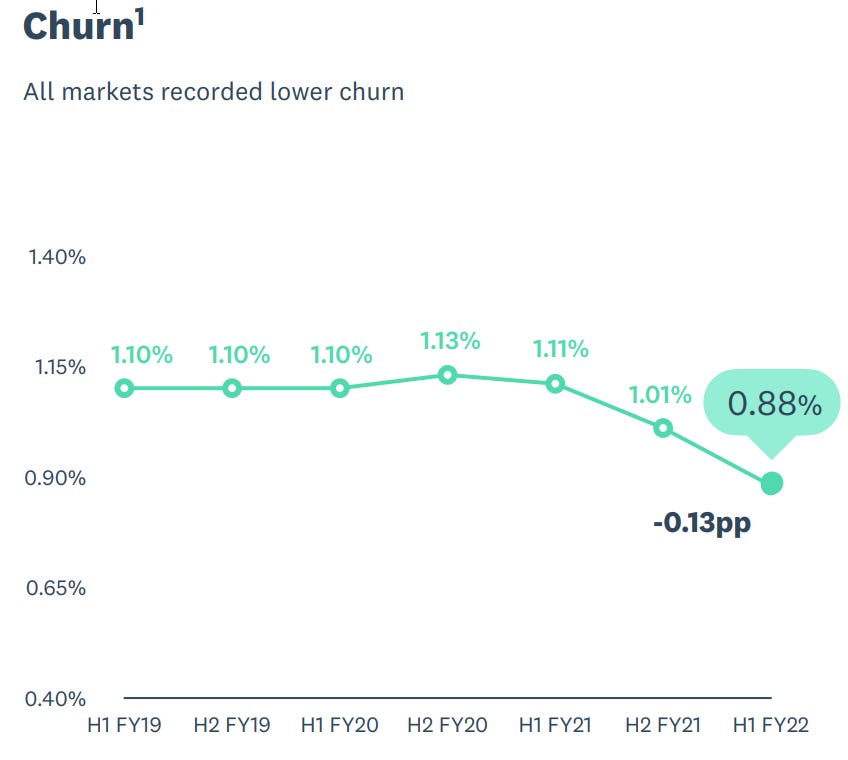

Churn

Low customer churn is an important feature of a SaaS business. It reflects a combination of low prices and high switching costs.

By example, Atlassian’s flagship product, Jira, has pricing that ranges from free to $14.50 per user, per month. There may be flaws in Jira, but at these pricing levels there’s no scope for a competitor to profitably emerge.

Similarly, over the last decade, Apple and Google have developed products that challenge Microsoft’s Office Suite but data storage and other switching costs have allowed Microsoft to remain dominant.

Xero’s churn has been low and has fallen further in the last year.

Customer Acquisition Cost

As the product matures, customer acquisition costs should tend towards zero. New users are attracted by the productivity benefits and expanding network effects. New starters at a business are automatically licensed, suppliers adapt to their customers needs, and competitors see the efficiencies gained by rivals.

There are two paths to zero.

The first is the digital native business. The digitally native model sells direct to the end user. The sales process will largely have been word of mouth from customers, suppliers and competitors. Xero, Adobe and Atlassian are examples. Atlassian, famously, doesn’t have a salesforce.

The second is through the C-Suite. Here there are large upfront, direct, sales costs through engagement with senior management. It’s convincing a company that a SaaS solution will improve the entire company’s productivity in a particular process. But once senior management is convinced, new license sales cost nothing. ServiceNow, SAP, and salesforce.com are examples.

The Result

These true SaaS companies with unique business models in the context of history are capable of unconstrained growth (the five in the chart below have averaged 30% CAGR since 2015) and rising gross margins (average 84%). The challenge, addressed in the next episode, is to understand what to pay for these businesses.