Aphorisms work: Not this time.

Aphorisms work: Not this time.

Rio Tinto, BHP and Fortescue are in a sweet spot of supply-demand dynamics, created by the Federal Reserve and aggressive tightening.

There’s a non-linearity to markets and economic behaviour that can often wrong-foot investors, experienced or otherwise. Part of the heuristic that allows for understanding is an aphorism1, such as “buy low, sell high”, “buy the dip (BTFD)” or “markets can stay irrational longer than you can stay solvent.” There’s a truth to these aphorisms but they’re not Gospel. The current macro environment highlights this.

Higher interest rates lower inflation. Not this time.

Earlier newsletters focused on the supply-side problems driving interest rates around the world. It argued that addressing supply-side inflation with interest rates would worsen income equality and leave the root cause unaddressed.

Hedge fund manager Hugh Hendry, who has changed his image recently (he now develops resort villas in St Bart’s) makes this point regarding Fed monetary policy in his Acid House Capitalist podcast.

His argument: monetary policy is too tight, and the constant demands to tighten policy at the first sign of inflation make it worse.

Hugh Hendry:

What would I do? I would take them on, I’d be like fire me (As Federal Reserve Chair). We’re in a depression (more on this one day), I ain’t raising rates. Let me talk you through the last twelve years where we tried this. It doesn’t work. And more than this I’m becoming culpable, … , my misadventures … in credit tightening may actually be one of the most prominent explanations for why commodity prices are very high today. If I pursue the Fed’s current path, the legacy of that error is going to be prolonged elevation of commodity prices.

He’s arguing that as rates rise, the incentive to produce more of something declines.

The cure for high inflation is higher prices. Not this time.

He illustrates his argument with BHP and Rio Tinto. Both companies, he argues, are disincentivised to invest in increased mineral production by the Federal Reserve’s monetary tightening cycles, of which there have been three in the last decade.

There are two profoundly large diversified mining stocks in the world, BHP and Rio Tinto, Rio Tinto yields 9% (actually 12.6%) … and is buying back its stock, it (the Fed’s tightening) has forced upon them, under no circumstances, should they mine for new material.

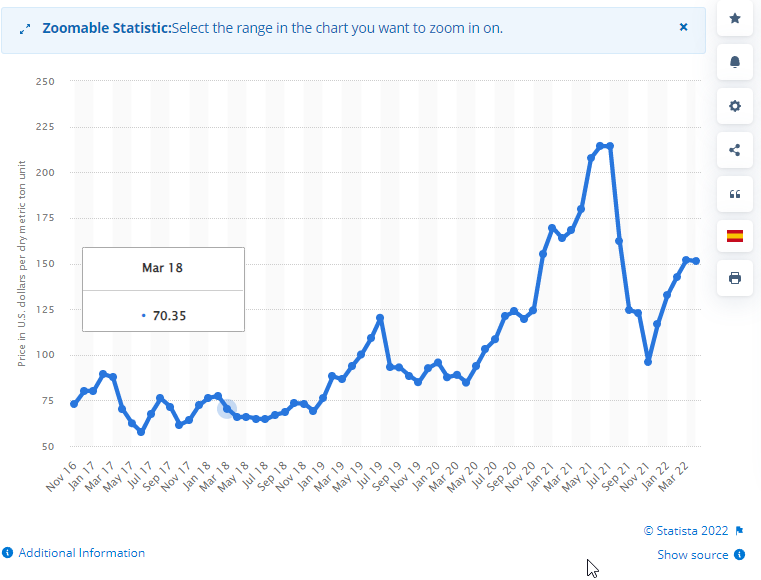

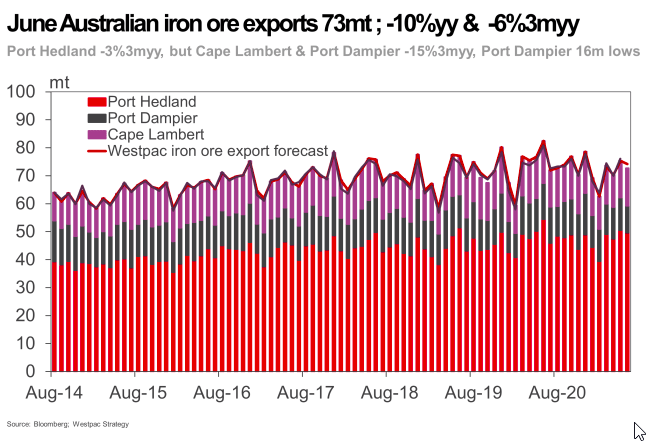

It’s an important observation. The fight against inflation is actively discouraging the higher supply that solves inflation. If Fortescue Metals Group is added to the list, it’s obvious that the large Australian miners are not adding supply to the iron ore market, even with elevated prices. Australian iron ore exports are broadly flat from 2017.

Iron Ore Prices.

Australian Iron Ore Shipments

Hendry also points out that as money becomes more expensive, or policy is tightened, the poor aren’t helped. It is profoundly unequal. As a Glaswegian, he leaves his ire for his own political left. He argues that the Guardian newspaper should be fomenting revolution at the lack of investment but instead it’s supporting tighter monetary policy and Extinction Rebellion’s policy of limiting investment in extractive industries.

Buy cyclicals on high multiples. Not this time.

From an investment perspective, it highlights that resources are an important part of wealth creation and protection in the current environment. The challenge is the timing.

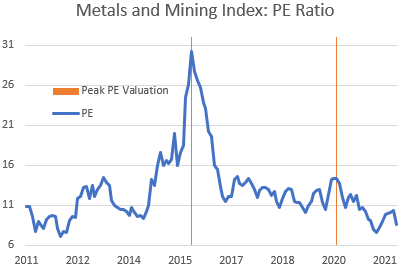

A resources investor “knows” the best time to invest is when PE ratios for resource stocks are high. This counter-intuitive view reflects the cycle of commodity prices. A low PE ratio reflects cyclically high commodity prices and vice versa. This chart of the Metals and Mining Index’s historic PE makes the point. If an investor purchased at the peak in the PE ratio of mining companies, 30.2x in April 2016, the investor would have made 117% on today’s price and 316% at the peak. An investment at the the 2011 PE low would (excluding dividends) be under water at current prices.

This time it’s different. It is.

This time is different. Resources should be a core part of a global equity portfolio. As Richard Fairbank argued of credit card consumers, people learn from difficult lessons and develop scars in the process. Between the scars of boards and investors, there is no appetite for risky expansion. Further, the industry structure has tightened so that only Australia plus Brazil can move the supply needle. There is no marginal supplier that can emerge and solve the market’s problem.

Hendry’s point is well made. High interest rates aren’t providing the incentive to encourage a supply response. This will be the case across commodities. Further, it will take years for companies to lose the scars of successive Fed tightening periods and expand production aggressively. Resources companies can only benefit from the dynamic.

“Not this time” is a market aphorism.