If Something is to Break, it won't be the US Consumer

If Something is to Break, it won't be the US Consumer

The US consumer is well positioned to absorb further Fed rate rises. It's the rest of the world, particularly Europe, that faces the steepest challenges.

The Federal Reserve may face a dilemma: US growth that is faster than they believe it needs to be, and an increasingly weak global economy.

There’s a sense that the Federal Reserve is determined to break the US economy. Commentary from the various Federal Reserve Governors points to a desire to crush inflation, regardless of the broader outcomes to the economy, employment, and financial markets. This reflects the belief that as actors within an economy become comfortable with inflation, it becomes difficult to slow the pace of price rises. It’s better to act sooner, than later.

Speeches Highlight Determination To Slow Inflation

Speeches in the last week have highlighted this. For instance, Fed Governor Christopher Waller said:

In considering what might happen to alter my expectations about the path of policy, I've read some speculation recently that financial stability concerns could possibly lead the FOMC to slow rate increases or halt them earlier than expected. Let me be clear that this is not something I'm considering or believe to be a very likely development.

I am a little confused about this speculation. While there has been some increased volatility and liquidity strains in financial markets lately, overall, I believe markets are operating effectively.

Similarly, Fed Governor Lael Brainard said that economic growth needs to moderate further, with the help of tighter monetary policy, to ensure inflation does not become entrenched.

The moderation in demand due to monetary policy tightening is only partly realized so far. The transmission of tighter policy is most evident in highly interest-sensitive sectors like housing, … In other sectors, lags in transmission mean that policy actions to date will have their full effect on activity in coming quarters, and the effect on price setting may take longer. The moderation in demand should be reinforced by the concurrent rapid global tightening of monetary policy.

The message from the Federal Reserve is clear, interest rate rises will continue, and growth must moderate further, regardless of the consequences.

How Far Does the US Economy Need to Break?

We think quashing inflation that quickly amid constrained production capacity would take a recession – a roughly 2% hit to economic activity and 3 million more unemployed.

Such a slowdown would reflect a recession greater than the Tech Wreck period, but less than the GFC. All of this makes academic sense, but reality comes with challenges. Is the US economy, particularly the consumer, ready to break? Will the global economy, excluding the US, break first?

Will Further Rate Rises Hurt the US Consumer?

As has long been the case, slowing the US economy requires a weaker US consumer. It’s not clear that further tightening of monetary policy will slow the US consumer.

First, for the time being at least, the challenges in supply chains are supporting employment growth. In September, the US economy created 263,000 new jobs: above the expectations of the market, and the desires of the Federal Reserve.

Second, households seem comfortable spending income. This is driven by employment, and an historically high savings rate through the period of the pandemic. Despite the current decline in the savings rate, it remains positive, and the stock of savings, measured below as bank deposits of households, are equivalent to 28% of annual household expenditure. These are levels of cash savings, relative to consumption, that were last observed in the 1950s. This is even more pronounced, given consumption is a larger part of GDP at 68%, compared to 58% in the 1950s.

Third, while policy tightening has had a noticeable impact on housing demand, further rate rises are likely to have less of an impact. Already, the spread between 30-year mortgage rates and the 30-year bond rate are higher than historical averages. This gives room for lenders to absorb further rate hikes to increase mortgage demand.

For households with mortgages already, around two thirds have a fixed, 30-year mortgage rate of less than 4%. There’s no vulnerability to rate rises amongst this cohort.

Fourth, the impact of higher short-term rates will begin to be outright beneficial to US consumers. Higher interest rates will strengthen the US dollar and slow imported price growth, reducing demand in the rest of the world to the benefit of the US.

What about the rest of the World?

The outlook for the rest of the world is considerably less sanguine. The consequences of aggressive monetary tightening in the United States are roiling financial markets and likely slowing demand elsewhere.

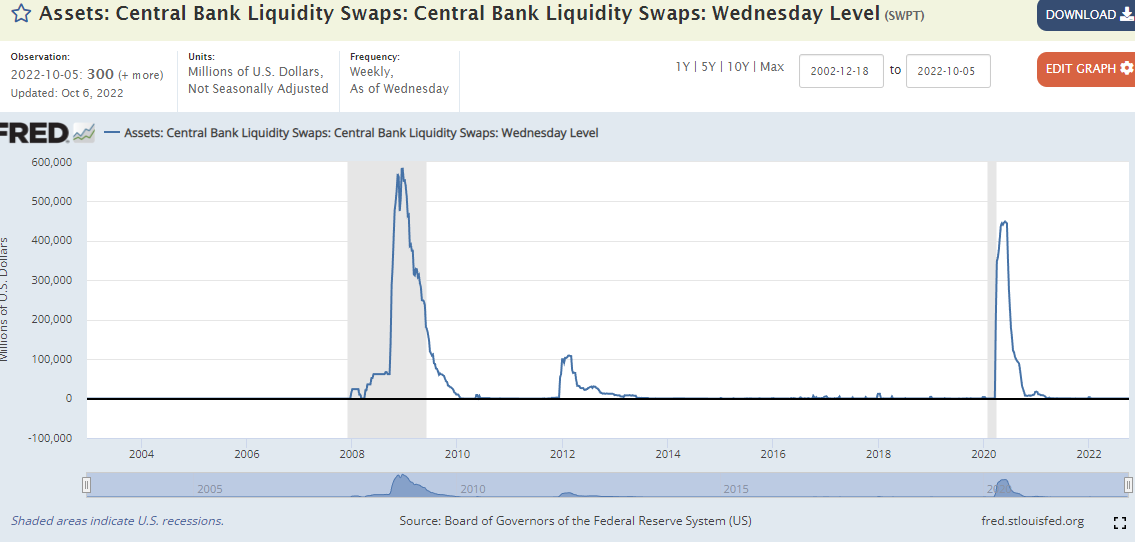

Indeed, there is some evidence that the Fed is relatively comfortable with this outcome. For instance, in the Global Financial Crisis when availability of US dollars fell, the Federal Reserve instituted swap lines with counterpart central banks with the aim of providing liquidity to relieve stress in markets. To date, as at 5th October, these swap lines have not been made available, and/or utilised. This seems surprising in light of the travails of interest rate markets, particularly the Gilt market in the UK.

The Fed will also have external assistance through the troubles in Europe. The chart below1, highlights the displacement of activity from Europe to the rest of the world. Europe is acting to stabilise prices, but also boosting activity elsewhere. The growth in external orders, points to stronger demand for manufacturing in both North America and Asia.

It could be argued that OPEC’s production cut, likely reflects some concern that European demand for oil will be considerably lower than current expectations.

By example, consider the construction industry. The construction industry accounts for one fifth of global oil consumption. If heavy industry, producing steel, bricks, cement, glass, and tiles, is shut down in Europe, the downstream impact on oil demand from construction activity will be substantial. Again, this external decline in oil demand will be positive for the US. This is but one example of weaker demand elsewhere, benefiting the US.

If the World Breaks, but the US Consumer Doesn’t?

It may be that the desire to break the US economy ends with the US consumer standing undefeated. In the examination of trends and forces facing the world’s economic powerhouse, there’s a likelihood of positivity, not negativity. That said, the impact on the broader global economy, particularly Europe, will be far from benign.

It will be fascinating (terrifying) to see how aggressively the Federal Reserve pushes the string of higher short-term interest rates and its impact on the global economy.

This environment, stable to growing US consumer, weaker Europe, and recovering Asia, forms the macro backdrop for portfolio construction.