Macro Monday: Lockdown 2.0

Macro Monday: Lockdown 2.0

Lockdown 2.0 will be more effective than the Federal Reserve.

Asset markets continue to be greatly concerned by inflation and a long policy tightening cycle by global central banks. Inflation is such a problem that only a sustained period of weaker demand, created by higher interest rates, can resolve entrenched price increases.

But is that the only solution?

Lockdown 2.0

An extreme, but likely solution to the problem would be a self-imposed return to lockdown. Just as the first lockdown saw an immediate dramatic decline in prices, a second, voluntary lockdown would lead to lower prices and a resumption of higher economic growth in the future.

This is the solution that markets are clearly driving for. By increasing prices on the global economy, markets are forcing a rapid decline in economic activity. As economic activity declines, a period of time when supply can begin to catch up will become available. This will help prices normalise in the medium term.

For instance, of the 35,000 flights scheduled for Sunday June 19th in the US, 916 were cancelled. It was over 1400 on Friday. As random as this may seem, cancelling 4% of flights leads to better dynamics in the stretched jet fuel market. In a similar vein, in a NFSW rant, a truck driver in the US shows packed truck stops, full of trucks unable to get diesel. Activity stops, it doesn’t continue at higher prices.

As discussed on Friday, the sharp increase in European energy prices, particularly natural gas (71% in a week), will lead to shut downs of economic activity. Manufacturing businesses cannot be profitable at these prices. Early summer holidays are on the menu. It may not be entirely coincidental, in this context of higher prices, that France banned outdoor events as a consequence of the heat wave. It forces lower economic activity.

The market created rise in 30-year mortgage interest rates is leading to a near-complete collapse in US housing activity. The chart below shows home listings in the Greater Phoenix area have doubled from mid-April 2022. At these mortgage rates, economic activity is unlikely to occur. This in turn, will put downward pressure on housing costs and inflation, until such time as it can resume more sustainably.

Finally, emerging market mobility data shows that across countries like Indonesia, India, Brazil, and Argentina transport activity growth has stalled, or even begun to decline. Prices are too high for these consumers to maintain previous levels of activity growth.

Will this be sufficient?

It’s likely that markets continue to push prices to the point where activity stops. At such price levels, demand will disappear, and allow supply a period of time in which it can catch up. The sharper the prices rises are, the faster this period can occur, and then pass. There should be no doubt that prices will reach levels that inhibit economic activity. A sustained decline in the oil price would indicate this point has been reached.

It’s likely to come to pass at a considerably faster rater than if the economy were to wait for monetary policy, as the Fed seemed to indicate last week.

The Federal Reserve

Last week the Federal Reserve raised interest rates by 75bps in an effort to slow inflation from its fastest pace since 1984. The expectation of markets is for another, similar sized move, to occur in July. The Federal Reserve, through its “dot plot” chart1, indicates that, in addition to the July move, rates will rise a further one percentage point in 2022, and 40bps in 2023, taking the Fed Funds Rate to 3.8% in 2023.

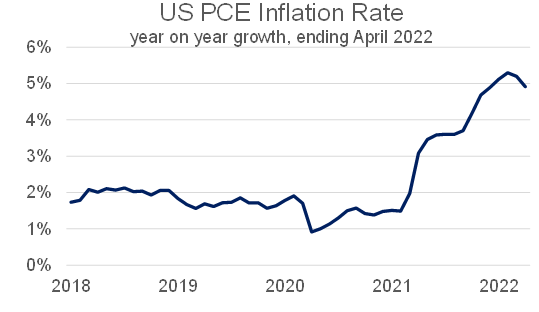

The Federal Reserve aims to have inflation under control by 2023. It currently forecasts inflation, using its favoured measure (PCE), at 5.15% in 2022 and falling to 2.70% in 2023. Interestingly, to reach its 2022 forecast, the Fed expects inflation to re-accelerate from the current 4.9% in April.

There are a number of points to make about the Fed’s policy position.

First, it is forecasting a re-acceleration in inflation, so as to justify aggressive policy action. If inflation peaked two months ago, as the chart currently suggests, aggressive action may not be as necessary, now. It would have, however, helped a year ago. To be fair, it wants its forecast (of high inflation) to be wrong.

Second, Jerome Powell, the Fed Chair, is clear that a large part of the problem is beyond the control of the Fed:

… supply constraints have been larger and longer lasting than anticipated, and price pressures have spread to a broad range of goods and services. The surge in prices of crude oil and other commodities that resulted from Russia’s invasion of Ukraine is boosting prices for gasoline and food and is creating additional upward pressure on inflation.

Monetary policy cannot resolve these problems. As has been discussed above, the market likely achieves the Federal Reserve’s goals first.

On the basis of this analysis, the Fed Funds rate peaks this year, and with a six month horizon, the market begins to price this in.

The Fed's dot plot is a chart that records each Fed official's projection for the central bank's key short-term interest rate.