Macro Monday: Structural Inflation

How should investors think about inflation in the long-term?

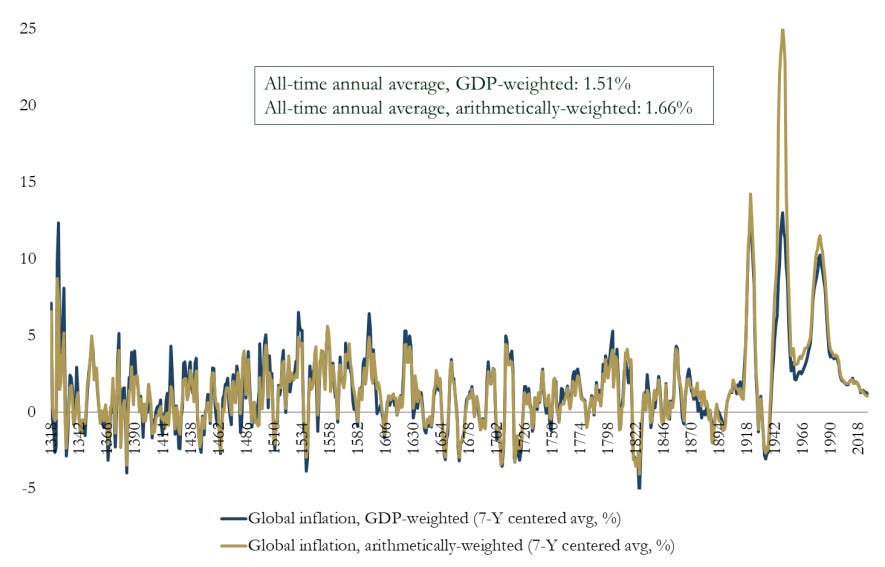

With inflation dominating market commentaries, it is useful to take a step back and think about inflation from a longer-term perspective. For many, a longer-term perspective of inflation and interest rates means the oil shocks of the 1970s. But fortunately, Paul Schmelzing of the Bank of England, has created an inflation and interest rates time series going back to the 1300s.

The History of Interest Rates and Inflation

Using records from royal courts, Schmelzing has pieced together interest rates and inflation data. His first conclusion, is that nominal rates were in trend decline well before monetary authorities came up with the idea of quantitative easing. In other words, the market has pushed interest rates lower over time.

A second conclusion, is that inflation is not a universal outcome over history; through the last seven centuries inflation has been closer to zero than 10%. Indeed, half the annual observations from 1311 to 1745 were negative1. The 20th century has been an outlier.

Inflationary periods have had a number of drivers. The success or failure of local harvests is particularly important. Similarly, spikes have been associated with war. As a large part of working age labour heads off to war, and governments commandeer produce to feed the army, prices rise. The inflation spikes associated with the Napoleonic Wars and the US Civil War are observable in these charts. The industrial scale of war in the 20th century is plain in these charts.

The two most recent spikes in inflation; the 1970s and the last two years might be explained by a similar dynamic. The War in Vietnam created the conditions for a decade of inflation, with further exacerbations from the oil crises. The once in a century pandemic of 2020/21 was similar in effect, the workforce was quarantined while, in many areas, demand remained constant (food, for instance).

Innovation not Inflation is the Natural State of Humanity

But generally, inflation has been low. In times of peace, for instance 1870 to 1900, and from 1981 to the present day (just), inflation trends down. This reflects two broad trends: continued innovation, and consumers’ ability to pay low prices. This newsletter discusses innovation.

The natural state of humanity, despite the negative amongst us, has been towards doing things better. As we improve, productivity improves and prices fall.

There’s the view that innovation is discrete events of invention and discovery. These events are the creation of great men and women who create step changes in the productivity of the global economy.

The last governor of the Australian RBA, Glenn Stevens, made a more nuanced argument. Innovation is an incremental process driven by individuals, all trying to make their job easier. (To paraphrase). In reality, it’s a combination of the two.

Three great inventions bear this out. All three came to being in a broader milieu of innovation. All three fundamentally changed human productivity, and consequently lowered prices, but often at a distance removed from the initial innovation.

James Watt’s steam engine in 1769. By adding a steam condensing chamber to his engine, Watt built a fundamentally more productive engine by building on the knowledge that was already in existence. Watt’s engine used 75% less fuel than contemporary engines. Interestingly, it took 100 years, with the emergence of big factories, for the steam engine to be properly harnessed.

Wright Brothers’ motor-operated airplane in 1903. Again, the innovation, a three way gear box, solving for pitch, roll, and yaw, enabled the Wright’s to succeed where others had not. But again, it took a while for the innovation to bear fruit productively. Partly, this was due to the Wright Brothers patent control on plane development. Innovation slowed greatly in the US, such that American fighter pilots used European planes in the First World War. It took until 1926 with the opening of the New York to San Francisco airmail route for airplane technology to bear productivity fruit.

Bessemer steel production. The process removed impurities from iron by oxidation with air being blown through the molten iron. It sped up the manufacturing process, created stronger steel, and used less resources. There’s evidence of this method in 11th century China, 16th century Japan, and 18th century Europe, and debate around whether it was truly Bessemer’s invention. It was initially aimed at improving the quality of steel used in cannons for the Crimean War in the 1850s. Its productivity benefit, however, came with mass production of steel in the 1870s and the building of America’s railroads.

As humans, we are capable of innovation, whether as individuals or collectively, as we are seeking to improve our lives. This raises living standards, and, over time, lowers inflation. There’s no reason to believe this process has ended.

The CPI basket was based on Northern Italian prices and includes the key food items, energy prices, linen, soap, and candles, and is based on institutional, urban price data, expressed in silver unit equivalents.

Fantastic post. My thoughts are you are correct about war-time leading to inflation, not just due to supply chain disruption but also the fact that wars are generally not popular - historically it has not been politically tenable to tax the population to fund wars so politicians turned inevitably to debasement of the coin. This is as true today with our fiat money system as it was when they clipped coins to fund the Crusades. Obviously the 20th century sticks out for its relative instability - it is easy to point at the wars but how much influence did the establishment of the Federal Reserve in 1912 have I wonder? If nothing else did it give humans the ability to fight wars on a global scale? It is clearly complex and one could argue technology has been the driver but since early 20th governments have been comfortable borrowing beyond their means, institutional banks have been comfortable lending large sums of government-guaranteed money to countries that will never have the ability to pay it back and as your graph clearly illustrates - 'boom/bust' has become the norm.