Macro: Three Assertions

Macro: Three Assertions

Hawks are Bulls, Shorts are Historically Crowded, and Inequality Rises.

Caveat.1

Here’s three assertions about the current macro environment.

The More Hawkish The Fed, The Better For Markets.

Flow Matters More Than Fundamentals.

Inequality Is Positively Correlated To The Equity Market.

The More Hawkish The Fed, The Better For Markets.

This weekend central bankers from around the world convene in Jackson Hole, Wyoming. The annual conference is an opportunity for central bankers to outline a strategic view of the global economy, and current policy framework, and settings.

There is concern, in the commentariat, that the Federal Reserve, through Jerome Powell, will commit to further aggression in the crusade against inflation. Indeed, in anticipation, the equity market has fallen up to 5% from recent highs.

In all likelihood, however, a renewed commitment to fighting inflation through policy adjustment (raising rates) would be viewed by the market as positive. This view reflects a number of dynamics.

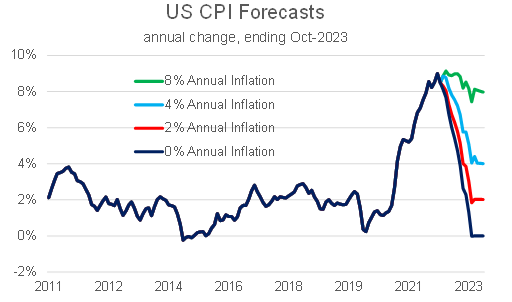

First, inflation is coming down. As the chart below shows, even with continued price increases (in the range of 4-6% annualised), inflation will have peaked in May/June 2022.

Second, an aggressive approach to short-term inflation management will provide the bond market with greater confidence over the long-term. This will lower long-term inflation expectations that have risen in the last month. Lower long-term bond yields support higher equity prices.

Flow Matters More Than Fundamentals.

A commentariat view is that market moves should reflect fundamentals. For the more pragmatic, it’s sensible to believe that markets are right twice a cycle, once on the way up, and once on the way down. Most of the time prices are relatively inaccurate.

The biggest contributor to this is financial flows. Some recent instances can highlight this.

This week the Saudis threatened to cut supplies of oil. The Saudis are of the view that the current financial market price does not reflect the tightness of the physical market. They believe the ebb and flow of financial traders has detached the price of oil from reality and intervention is required to return prices to fundamentals.

Similarly, in the last fortnight, the world has learned of Jake Freeman’s $110 million profit trading Bed, Bath and Beyond. Freeman’s initial $25 million investment quintupled in the space of six weeks as WallStreetBets’ momentum took hold of the stock. Again, fundamentals had nothing to do with price moves.

But perhaps, the most pertinent example of this comes in the S&P 500. It may be that there are no sensible reasons to be buying equities at this point in the economic cycle. But, similarly, there are even fewer sensible reasons to sell equities at this point in the price cycle.

The coronavirus pandemic period highlights this well. The futures positions of traders were peak negative in March through May 2020. By May, the S&P 500 was approaching its previous all-time-high. Simply, rather than fundamentally, there was no one left to sell the market, and the constant buyers, pension funds etc, were pushing prices higher.

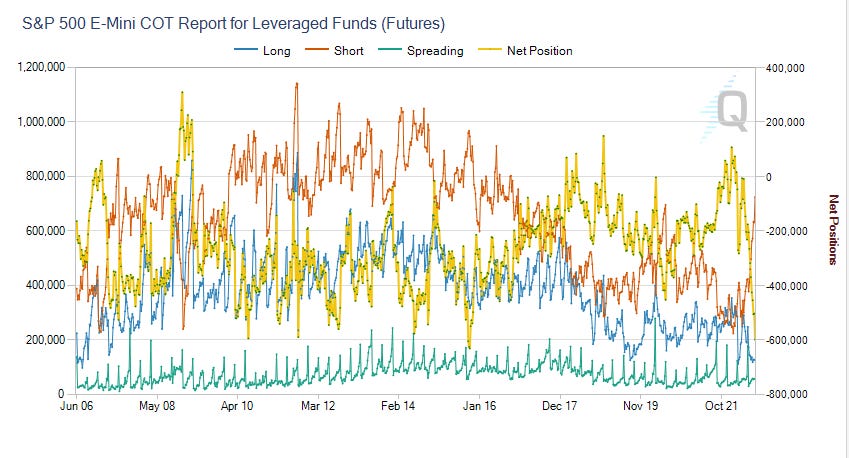

It’s similar today. There’s no one left to sell. The terrible (formatted) chart below, shows the market is shorter today, than during the pandemic phase. The net position (longs minus shorts) is at historic extremes (more aggressive than in the pandemic). The longs are at historic lows. To be negative on the market is to be market consensus when the consensus is at historic extremes. That’s not a winning position.

Inequality Is Positively Correlated To The Equity Market.

In the course of 2022, as equity markets rally towards all time highs, the pain felt by ordinary people, and the European Union collectively, will be extreme.

Prices will remain high, and some demand will come out of the US economy. Employment and wages will be negatively impacted. The toughest times will be faced by those least able to afford it. But the better off people are, the easier it will be to remain insulated from the pressures of rising prices. Indeed, insulating oneself from price pressures could support parts of the market.

Tesla. As oil prices rise, remain high, the economics of driving an electric vehicle improve. The better off a household is, the easier, and more productive, the shift to an EV becomes. Less well off households will remain exposed to rising oil prices. Tesla can do very well without expanding its market towards lower income households.

Europe, collectively, will have an even tougher time. In recent days, Azoty Group in Poland and CF Fertilisers in the UK have announced production suspensions due to a lack of CO2. Carlsberg are talking of suspending beer production for similar reasons. With energy prices touching $1,000 per barrel of oil equivalent in Europe, it’s likely that shutdowns of industry will occur.

Again, it won’t necessarily slow the US equity market’s gains.

Indeed, it should be expected that Europe’s woes will benefit the US. CEO of Cleveland Cliffs, Lourenco Gonsalves highlighted the opportunity in July:

… the reality is sinking in, in Europe. … They don’t have natural gas even to heat their houses. So we are starting to see reallocation of microchips and other things from Europe to the United States.

Planned European production will increasingly be transferred to the US. In coming months, there should be an improvement in US industrial production, particularly of new orders for fertilisers and chemicals, and an improvement in bulk shipping rates, as this transfer occurs. Again, this will benefit US equities.

One has to wonder at what political cost a rally in equities will have in coming years and electoral cycles.

Conclusion

In the next six months, the contradiction of markets and economies will be stark. The real economy will remain beset by the tail end of high prices caused by pandemic dislocations, and the war in Ukraine. But financial markets will begin pricing in both the end of these dislocations, and lower interest rates. It will be quite the contradiction.

The assertions are thought experiments reflecting a higher probability outcome than the alternative. As a long-only investor, it would be better if equities went up. The Lessep portfolio, however, is not going to change substantially, if at all, on this macro assessment. The portfolio is twenty individual ideas, often with idiosyncratic drivers, and 114 stocks (the bottom 17 make up just one per cent of capital).