Last week’s Macro Monday explored inflation over time. It argued that war was a big driver of inflation over history. It also argued that innovation, doing more with less, has been an important contributor to lower inflation.

This week a further factor is considered; consumers only pay what they need to pay. This may seem an obvious statement but it’s important in the context of understanding inflationary dynamics. In particular, why has easy monetary policy not created higher inflation?

Again, it’s useful to put this in the broader historical context.

Inflation in the 20th Century

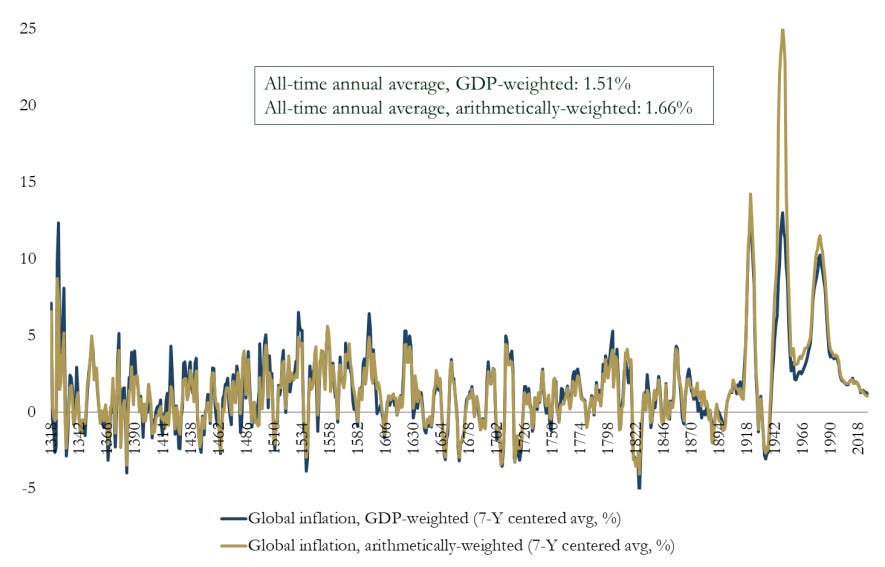

As discussed last week, inflation in the 20th century stands out as being higher, typically, than at any other period in the last seven centuries. One obvious, and tragic, answer for higher inflation is the industrial scale of war in this period.

In the absence of war, with its negative impact on supply, humans tend towards doing more with less. This allows price growth to remain low.

There may, however, have been another driver of structurally higher prices in the developed world over the 20th century. The ability to compel consumers to pay higher prices.

The Role of Branding

The period between 1870 and 1900 has been labelled by economists as the Long Depression. It is a fascinating period, detailed contemporaneously by David Ames Wells in his book Recent Economic Developments, of 1890.

The book details a period of deflation or disinflation, the Depression part, but also strong growth in economic activity and real living standards. Ames Wells believes that technological improvement created the dynamic. The world learned to do more with less.

For modern readers, a jarring aspect of the book is the use of the word commodity. For Ames Wells commodity is interchangeable with goods, including manufactures, as opposed to the contemporary definition: a raw material or primary agricultural product.

This may provide insight into 20th century inflation. In a market where everything is a commodity, the pricing power of firms is low. As commodities become branded goods, pricing power for firms increases.

An NGRAM search via Google (looks at the number of times a word is used in a year, relative to all words used in that year) of the words marketing, and trademark1 shows marketing emerges at the beginning of the 20th century. Firm pricing power was created in the 20th century, and likely increased prices, all things equal.

How does branding create inflation?

Brands create pricing power. Consumers are prepared to pay more for a branded good than a non-branded good.

The American travel writer, Bill Bryson, wrote Notes from a Big Country in the 1990s. It details his return to America after years in the United Kingdom. The passage below highlights the ability of brands to compel consumer behaviour:

“Holiday Inn, for instance, went from 79 outlets in 1958 to almost 1,500 in less than 20 years. Today, just five chains account for one-third of all the motel rooms in America. Travelers these days don’t want uncertainty in their lives. They want to stay in the same place, eat the same food, watch the same TV wherever they go.

I … got the idea that we should stop for the night at an old fashioned family-run place … Well we looked everywhere. We passed scores of motels, but they were all part of national chains. Eventually, after perhaps 90 minutes of futile hunting, I pulled off the interstate for the seventh or eighth time and – lo! … there shining out of the darkness was the Sleepy Hollow Motel, a perfect 1950s sort of place.

It was awful, of course. The furnishings were battered and threadbare. The room was so cold you could see your breath.

“It’s got character” I insisted.

“It’s got nits,” said my wife. “We’ll be across the road at the Comfort Inn”.”

This one anecdote summarises a brand’s power to influence prices and sustain them at a level that is higher than may be found in a competitive market. The brand works to exclude competition.

Legal Detour

The first trademark laws in the US came into being at the beginning of the Long Depression, 1868-1870. Interestingly, they didn’t work. The laws protected US brands offshore, and vice versa, but did not offer the same protection onshore. It was only in 1946 with the Lanham Act that trademarks received domestic protection.

Change Emerged in 2000

Two factors emerged in the 2000s that fundamentally changed the power of brands: China entering WTO and the Internet 2.0.

China

China has taken a less regulated approach to brands. In 2010 it was possible to visit a Wu-Mart Supermarket in Beijing and see toilet paper from H.K. listed company Vinda, and unlisted company Yinda on the same shelf. Similarly, between October 2005, and February 2011, the price of an LCD television fell 90%. It was competition from China that enabled the benefits of innovations, and scale to be passed on to consumers, rather than held as profit margin by producers.

Internet 2.0

As discussed in the Metaverse, Internet 2.0 enabled user-generated content, and user-generated content, particularly via the smartphone, enabled reviews. Reviews enabled small brands, or even standalone businesses, such as the Sleepy Hollow Motel, to compete more effectively with branded goods and services. The competition lowered prices, or increased quality. Of course, the internet also greatly improved price discovery.

Inflation is not a Monetary Phenomenon

The combination of increased competition and information enabled consumers to enjoy considerably better prices than had been the case for most of the 20th century.

The emergence of China and the internet as deflationary forces highlight an important dynamic. The monetary policy easing of the last decade, until the pandemic, failed to create high inflation. The expansion in money supply did not spawn run away prices. In this sense, the conditions did not exist, to compel consumers to spend more than they needed to for goods and services.

This leaves commodities as the driver of higher inflation. Commodities are unlikely to support broad-based, higher inflation, over a multi-year period (more than two years). Higher commodity prices should lead to an increase in the production of the commodity. High commodity prices will also, lead to deflation elsewhere, as high prices stop economic activity. Qantas cutting domestic capacity by 15 per cent until October, and 10 per cent thereafter, is a great example of high prices slowing activity.

The phrase JFK is added to provide context. It’s not until the late fifties that JFK is seen books.