The EM Big Wave Opportunity

The EM Big Wave Opportunity

Emerging Markets may represent the best investment opportunity in Global Equity Markets.

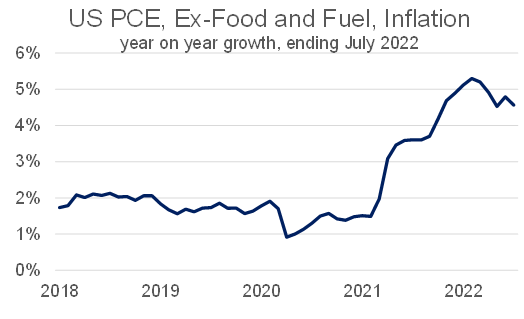

Jerome Powell’s recent speech at Jackson Hole seems to have stunned the equity market. Equities are down close to 4%, depending upon the benchmark. It hasn’t stunned the bond market. The US 10 year bond yield was broadly flat on Friday, and only slightly weaker on Monday, despite Powell’s comments. This is likely an indicator of things to come; the bond market is comfortable that, at this stage, the Fed has inflation under control. Indeed, PCE Inflation Ex Food and Fuel, also released on Friday, increased 0.1% for the month of July, and 4.6% year on year, the slowest monthly rate of increase since January 2021. There’s evidence inflation has peaked.

If further evidence of slowing inflation becomes available in coming months, the equity market will soon share the bond market’s sanguinity. It will see that the “data driven” Federal Reserve will begin, again, to support markets by slowing or stopping the tightening process. With this in mind, it’s worth considering the opportunities that may emerge. One opportunity stands out: Emerging Markets.

Market Pricing

As Callum Thomas highlights, emerging market equities have underperformed the S&P 500 since 2012, as growth concerns in China emerged. The under-performance is at historic extremes. Coupled with a very strong US dollar, and higher market interest rates, the macro environment for Emerging Markets could not be weaker.

But a reversal of the market’s extreme pricing, particularly as inflation shows signs of retreat, would offer a degree of relief for Emerging Market assets. The challenge would be in creating a more sustained improvement in the outlook for emerging economies. This is outlined below.

Economic Opportunity

The first catalyst for an improvement in emerging markets companies will be an acceleration in emerging market growth. The principal driver of this improvement will be displacement of economic activity from Europe to Asia and the Americas. As mentioned on Friday, there’s already evidence1 that the US is seeing higher economic activity from European dislocation.

Emerging markets should also benefit. For instance, the EU re-engaged with Brazil in the last week to accelerate signing of the Mercosur Trade Deal. The Irish Independent argues that this was driven by the Ukraine conflict:

Despite this, Brazil’s emergence as an ‘agricultural powerhouse’ amid the ongoing war in Ukraine is reported to be the rationale behind the EU’s return to the talks.

S&P is reporting that polymer exports from Asia are ramping up.

As factories shut down in Europe due to energy costs, it’s likely that Asia and the Americas will need to increase capacity to meet global demand. This will likely first occur in key manufactured bulk commodities such as fertiliser, chemicals, plastics, refined metals, and steel. This may be a sufficient catalyst to generate a rebound in economic activity amongst emerging markets.

It’s also likely that, in line with this recent newsletter, internal stimulus is coming in China. A recent $29 billion loan package aimed at property developers struggling to construct pre-sold property has not instilled confidence in the market. It’s believed that the package’s guarantee is insufficient. It may be that China’s monetary authorities need to come up with a “whatever it takes” moment. This would be very positive for emerging equities.

Emerging Markets Are Ready for Intervention

A second catalyst may be that the operating regime for developed and emerging industrial companies is slowly merging. As energy and supply chain pressures impact inflation and real household incomes, it may be that developed government intervention in markets increases. This tweet below outlines the argument.

This tweet cites the royalty increases imposed on metallurgical coal by the Queensland state government and an export ban on refined products from the US. In the last week, Energy Secretary Jennifer Granholm wrote to US based refiners asking for them to scale back exports of refined product to Europe.

The Wall Street Journal reports that in a letter to refiners, Granholm stated:

“Given the historic level of U.S. refined product exports, I again urge you to focus in the near term on building inventories in the United States, rather than selling down current stocks and further increasing exports,” she writes.

“It is our hope that companies will proactively address this need,” she adds. “If that is not the case, the Administration will need to consider additional Federal requirements or other emergency measures.”

It’s likely that European governments and regulators will issue similar edicts or encouragements to their own companies in coming months.

This does make emerging market companies, with long-term state intervention or regulation built into business models, relatively more attractive.

For instance, Vista, a portfolio holding, is constrained by government enforced domestic pricing. This limits the price of oil sold domestically to US$63 per barrel compared to $99.6 per barrel in the export market. Exported barrels make up 42% of all production.

Rather than an emerging market quirk, it might become a feature of developed economy companies too. This would close some of the valuation gap between a company like Chevron, and Petro Brasiliero, for instance.

A Lot Has Already Been Thrown at Emerging Markets

The last decade has been a period of adjustment for emerging markets. Since 2012, emerging markets have struggled. This has reflected a number of themes.

First, China has been a challenge for these economies. China’s slower growth has led to a decline in capital available for commodity investment in emerging markets. Most new commodity investment has been concentrated in developed economies. China has also maintained and expanded its dominance in manufacturing. Historically, rising wages in China would create opportunities amongst its peers. But China’s productivity, through scale and technology, has denied them this opportunity.

Second, volatility in monetary policy has generated a period of rolling crises through emerging economies. It began with the taper tantrum of 2014, again in 2018, and has afflicted these economies in 2022.

Finally, Covid’s impact on economic activity has, as with the rest of the world, been severe. For most emerging economies, with weak balance sheets, the period has been particularly destructive.

Can more be thrown at these economies? Have they begun to build internal resiliency? There is some evidence to say they are more capable of coping with external stress than has historically been the case.

Conclusion

The time for action in emerging markets has not yet arrived. Further confirmation of peaking inflation and economic activity being transferred to Asia and the Americas is required. But it is worth beginning the process of due diligence. How can investors get the best exposure to emerging markets, particularly when the index is dominated by Chinese technology?

Indeed, it should be expected that Europe’s woes will benefit the US. CEO of Cleveland Cliffs, Lourenco Gonsalves highlighted the opportunity in July:

… the reality is sinking in, in Europe. … They don’t have natural gas even to heat their houses. So we are starting to see reallocation of microchips and other things from Europe to the United States.