Software: Introducing Revenue Beta

Software: Introducing Revenue Beta

The stability of software revenues is worth something.

The Software 101 series has walked through the way Lessep thinks about software:

This newsletter will add to the valuation model by considering volatility.

Volatility in financial valuation

The foundational CAPM (Capital Asset Pricing Model) uses price volatility, measured in the form of price beta (the volatility of an asset relative to the broader index), to assist in the valuation of financial assets. The higher a company’s beta, the lower the valuation, all other things held constant.

Price volatility is useful for two reasons. First, the more volatile an asset’s price, the harder it becomes to hold the asset, increasing the probability of selling at a loss. Second, price volatility is associated with the underlying fundamentals of a company. Cyclical companies, with higher volatility in prices received and paid, and volumes sold, will have higher price beta as the market digests changing dynamics.

But as long-term, strategic investors, price volatility should be less of a concern. Instead, price volatility can be used as a tactical opportunity and the valuation focus remain on underlying fundamental valuation.

Revenue Beta

Anyone who studies SaaS companies will understand the predictability of their fundamentals. The challenge is assigning value to predictability. As a consequence, Lessep coined the idea of revenue beta1. The concept is simple; how volatile are a company’s revenues, relative to the revenues of the broader market. The lower the volatility, the higher the potential long-term valuation. SaaS companies have very low revenue betas, as low as 0.2. This low volatility justifies higher long-term valuations.

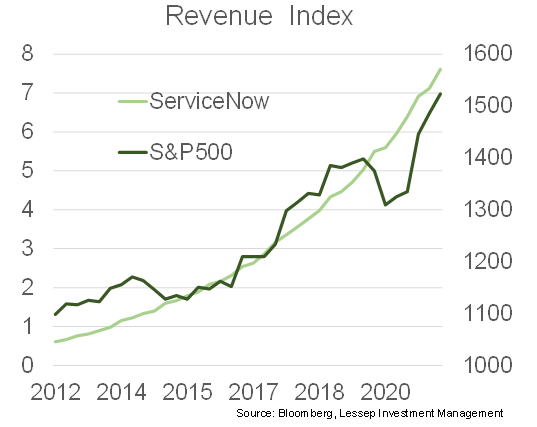

Again using ServiceNow, it’s possible to gain a visual representation of revenue beta. The chart below shows ServiceNow’s quarterly revenue relative to the revenue of the S&P500.

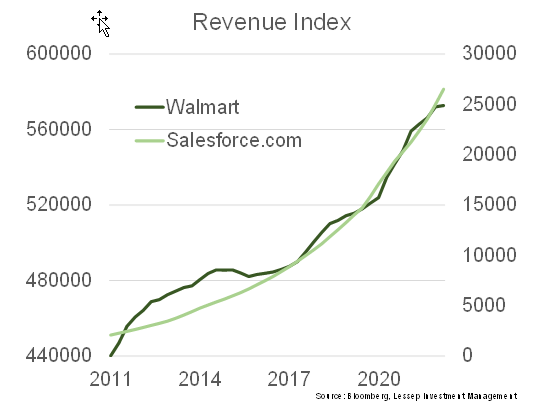

The next chart compares a traditionally low beta company, Walmart, with salesforce.com’s revenue. Again, the SaaS company with high price beta, fundamentally outperforms a core low beta company.

The stability of SaaS’s revenues justifies higher long-term valuations.

Why are these revenues so stable?

Generally, SaaS revenues are stable because the low point for the year is the high point of the prior year. SaaS businesses provide a compelling productivity proposition. If a service delivers productivity efficiencies, businesses will continue to pay the subscription. The alternative is higher costs.

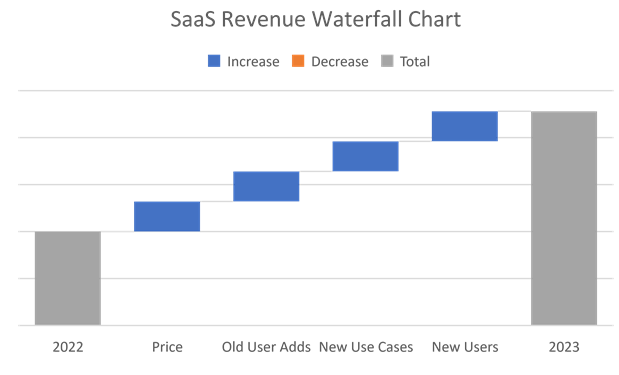

From the previous year’s high point, the SaaS business has four long-term drivers of revenue growth.

Price: An essential service has pricing power.

Old User Adds: Existing clients will grow their own businesses and subscribe for more employees.

New Use Cases: The SaaS company can identify new use cases for its software or identify where clients are using the software in a novel fashion. “Process mining” using big data analysis is a key area of growth for SaaS companies.

New Users: The sales process continues. Sales into mature corporations can be a laborious task delayed by bureaucracy, inertia, and identifying the key decision makers. Over time, SaaS companies penetrate further into the addressable market.

Adding Volatility to the Valuation

This analysis of fundamental volatility within SaaS companies can inform the valuation of the companies. It is another layer in the valuation process.

For Lessep, the stability of underlying revenue growth within SaaS companies allows for more accurate understanding of the future. This lower level of uncertainty, decreases the discount rate, and increases the potential return.

Valuation from last week with a 10% discount rate:

Valuation with an updated discount rate of 7.5%:

The final piece in the valuation jigsaw can be thought of as “the demand for equity” and will be discussed next week.