Software: Demand for Equity

Software 101: Episode 6

The Software 101 series has walked through the way Lessep thinks about software:

This newsletter will add to the valuation model by considering the demand for equity from SaaS companies.

The Demand for Equity

Historically, listing companies on stock exchanges served as a means of easily accessing equity finance. On-tap equity is essential for most businesses as they look for growth capital, make acquisitions, and seek to survive cycles. But today’s software companies, the survivors of the market’s weathering process, described by Bill McDermott1, no longer need new equity capital. Software companies are immune to these demands.

All things being equal, this low demand for equity capital, should lead to higher, long-term valuations.

Cash Generation

The cash generation of software companies is phenomenal. The chart below outlines growth in cash from operating activities over the last full three year period for a selection of global SaaS companies. It shows three year growth of between 15% (Microsoft and Intuit, companies that have a long history) and 55% and FCF yields of between 1% and 3.2%.

Make Acquisitions

SaaS companies have a fly-wheel of growth, outlined here, that allows them to grow rapidly and organically. Often companies are able to identify small, bolt-on, acquisitions that add to the product suite, but these can be funded from free cash. Alternatively, because of the monopolistic nature of software companies, regulators are unlikely to approve outcomes such as accounting software giants Xero and Intuit merging, or the merger of design duo Adobe and Canva.

The exception to this rule has been salesforce.com (CRM). CRM has made three large acquisitions: Slack for $27.7billion, Tableau for $15.7bn, and Mulesoft for $6.5bn. The strategic intent seems to have been to make CRM more useful to its clients, integrating it into processes beyond sales, towards marketing, customer service, data visualization, and workflow. Consequently, CRM has more debt than the average SaaS ($10bn), and a lower valuation (see FCF yield above).

SaaS Cycles

There are two ways to look at this. First, revenue beta highlights the limited impact economic cycles tend to have on SaaS companies. Second, even if SaaS companies suffered revenue declines in economic cycles, their clean balance sheets, generally net debt free, would make them immune to equity calls. Either way, the nature of SaaS companies excludes them from vulnerabilities to cycles and consequent capital raisings.

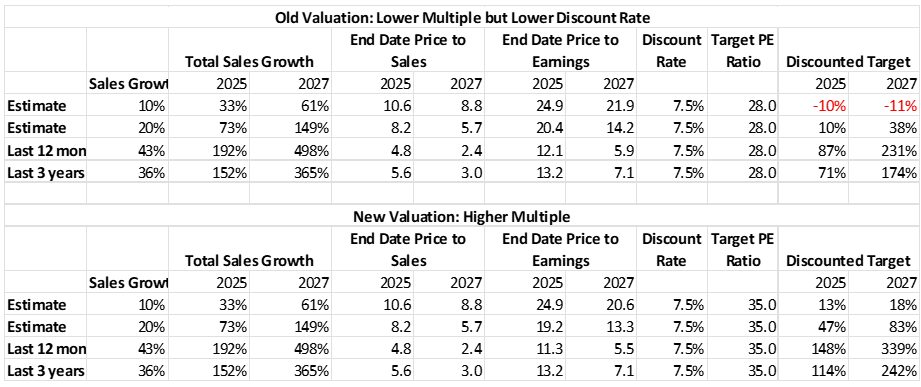

SaaS demands a Valuation Premium

SaaS companies are not traditional users of stock exchanges. They, generally, don’t need to raise equity capital. Their listing reflects an opportunity for founders, and venture capital to recoup the original investment, and to remunerate staff. Consequently, a SaaS company should trade at a valuation that is a multiple of those applied to either value, cyclical, or traditional growth companies. If this logic is applied to the ServiceNow model from previous episodes, it would justify an increase in long-term valuation from 28x to 35x. Clearly, higher valuations look absurd in the current market, but as longer-term investors, it should be possible to realise these prices.

“Since 2000, there were 4,500 companies in the IT industry that took a Series A investment, only 75 made it to an IPO, only 36 became dominant category winners. Those winners now own 76% of their entire addressable market…”